IndiGo IDFC FIRST Dual Credit Card Review 2025: Is ₹4,999 Fee Worth It?

Detailed review of IDFC FIRST IndiGo Credit Card: Compare benefits, milestone rewards, forex charges & application process. Best for IndiGo frequent flyers?

CARD REVIEWS

Kapil

11/8/20255 min read

IDFC FIRST Bank closed its Club Vistara credit card in March 2025 after the Vistara-Air India merger. Now they’ve partnered with IndiGo for a replacement. Makes sense on paper. IndiGo flies to 120+ destinations with 61% market share. Air India post-merger covers 90+ destinations with Vistara’s network absorbed. Both airlines now match each other for domestic reach.

But does this new IndiGo card fill the Vistara-sized hole in your wallet? Let’s find out.

BluChip Rewards: How Much Can You Actually Earn?

IndiGo launched its BluChip program in August 2024 alongside business class seats (called IndiGo Stretch). The airline finally caught up with competitors by offering a loyalty program and wider seats after 18 years. CEO Pieter Elbers called it “the fastest way to earn” with no blackout dates.

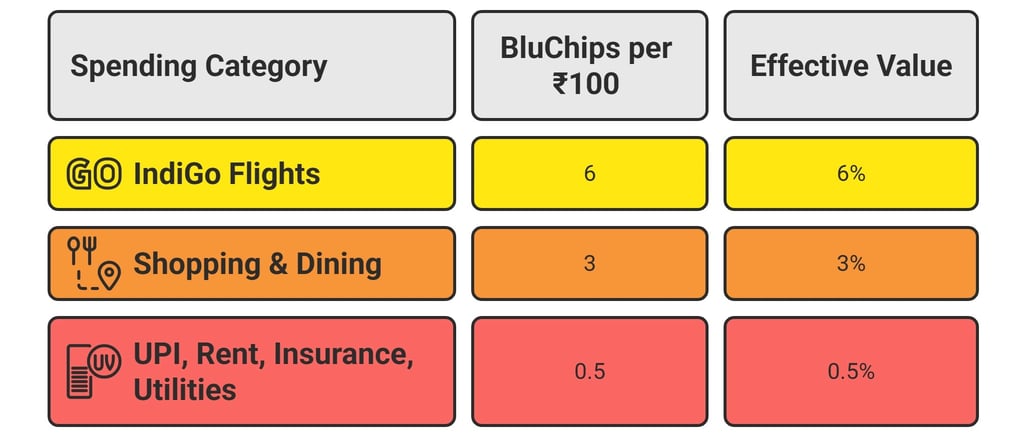

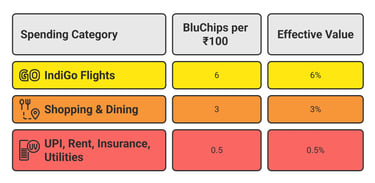

With this card, you earn 6 BluChips per ₹100 on IndiGo flight bookings. That’s a 6% return in flight currency.

Other spends vary wildly. Groceries and shopping: 3 BluChips per ₹100. UPI, rent, utilities, insurance: just 0.5 BluChips per ₹100. That half-percent rate kills most of your everyday rewards.

Each BluChip converts to ₹1 in flight value.

Real example: Your family spends ₹45,000 monthly (groceries, bills, fuel, shopping) plus ₹40,000 yearly on IndiGo tickets. Total: ₹5.8 lakh annually.

Base earnings: 12,600 BluChips from regular spends + 2,400 from flights = 15,000 BluChips (₹15,000). Add two milestone bonuses (at ₹2L and ₹5L spend) for 10,000 more BluChips. Grand total: 25,000 BluChips worth ₹25,000.

Subtract the ₹900 net fee (after welcome voucher). You keep ₹24,100. Return rate: 4.16%.

Milestone Bonuses Sound Great (But Do They Work?)

The card offers five milestone vouchers: spend ₹2L, ₹5L, ₹8L, ₹10L, or ₹12L and earn 5,000 BluChips each time.

Maxing all five gives 25,000 BluChips (₹25,000). That needs ₹12 lakh annual spend. That’s ₹1 lakh monthly. Tough for most families.

But here’s where it gets interesting. At ₹5.8 lakh spend, you hit two milestones. That’s ₹20,000 in bonus BluChips alone.

IndiGo’s loyalty program has three tiers. Blu 3 is basic with no bonus. Blu 2 needs ₹1 lakh flight spend plus four trips – unlocks 2 extra BluChips per ₹100 on tickets. Blu 1 needs ₹2 lakh plus eight flights – gives 4 bonus BluChips.

If you reached Blu 1 status with ₹40,000 flight spend, you’d earn 1,600 additional BluChips (₹1,600) annually. Return bumps to 4.43%. That’s genuinely competitive.

Real Value Behind the ₹5,000 Annual Fee

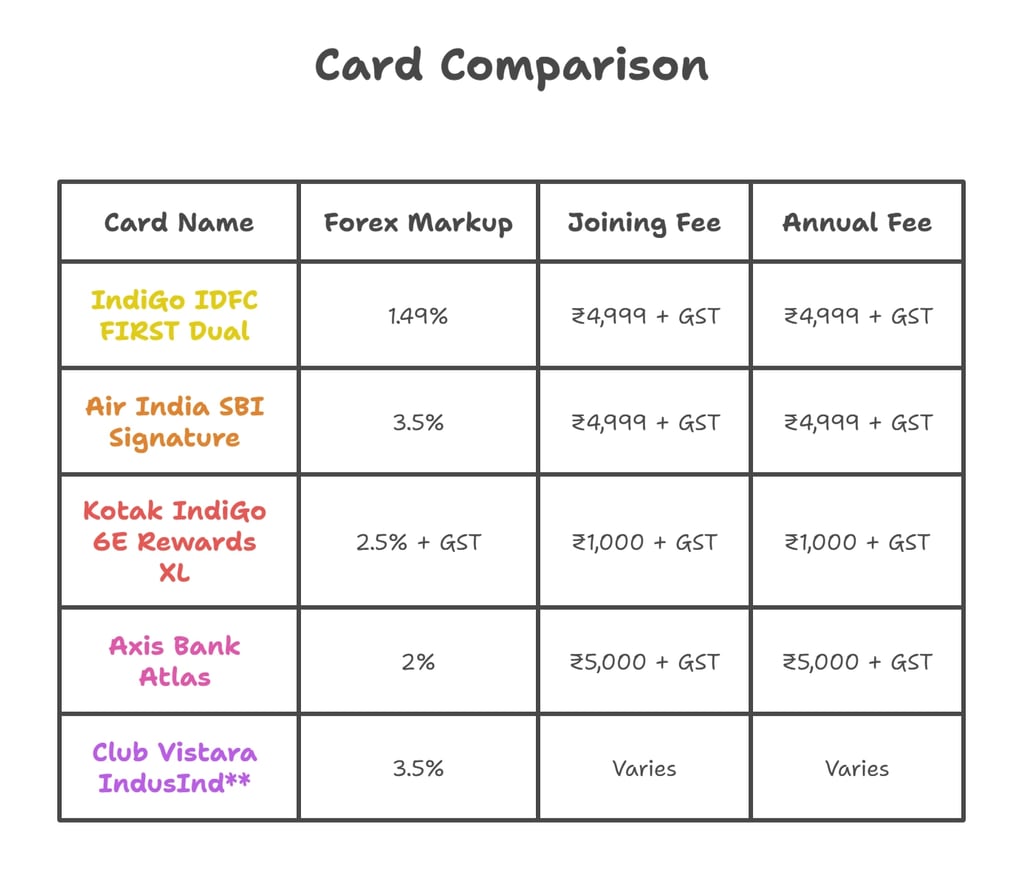

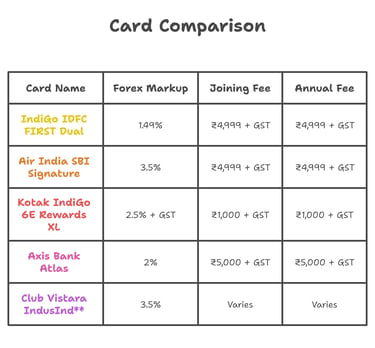

The card costs ₹4,999 plus GST. That’s ₹5,900 in year one. Steep for most wallets.

You get two cards: Mastercard for global use and RuPay for UPI. The Mastercard charges just 1.49% forex markup abroad. RuPay handles UPI at home.

Welcome benefits include 5,000 IndiGo BluChips (worth ₹5,000; considering you will redeem for flight booking on Indigo’s website) and a meal voucher. Net first-year cost: around ₹900.

Year two onwards? Same ₹4,999 fee. Same 5,000 BluChips. No waiver option. That’s a permanent ₹0 annual drain after factoring in vouchers (actually you come out ahead).

Alternative route: pledge a ₹1 lakh fixed deposit for zero joining fee. Credit limit equals your fixed deposit amount. Catch? You skip the 5,000 welcome BluChips in year one. From year two, everyone pays ₹4,999 regardless. At current fixed-deposit rates at 6.5% – 6.8%, one can easily offset more than the fees charged.

** Club Vistara Card is shown for comparison purposes only.

While most airline credit cards in India charge 3.5% forex markup, this one hits you with just 1.49%.

What does this mean in real money? Spend $1,000 abroad (about ₹83,000). With a 3.5% markup, you lose ₹2,905. With 1.49%, you lose just ₹1,237. That’s ₹1,668 saved on one trip.

Take two international trips yearly at $1,000 each. You save ₹3,336 just on forex charges compared to standard airline cards.

Why This Travel Card Skips Airport Lounges

Here’s the biggest letdown. Zero lounge access.

IDFC’s own Select and Ashva cards include lounge visits. But their flagship airline co-brand skips it entirely. Instead, you get 12 annual golf rounds. Because everyone’s suddenly into golf.

For a ₹5,000 travel card, missing lounges is bizarre. Most competing airline cards offer 2-4 quarterly visits minimum.

Still, at 4%+ returns, you can afford to buy occasional lounge passes out of your rewards.

It appears IndiGo likely skipped lounge access to control costs. With highest market share, the airline targets frequent flyers already using IndiGo – offering lounges would create recurring expenses for people switching from other cards.

However, there is a good chance of adding at least one complimentary quarterly visit in the coming future which shouldn’t hurt from the cost front and could make this card genuinely competitive with other premium airline offerings.

Who Should Actually Apply for This Card?

Get this if you fly IndiGo 3-4+ times yearly and spend ₹5 lakh+ annually. The dual-card setup works well: Mastercard abroad, RuPay for UPI. At 4%+ returns, this card delivers real value.

Skip it if you barely fly or have under ₹3 lakh annual spend. The reward potential needs volume to shine.

FD option helps credit newbies building history. At these return rates, it becomes a legitimate wealth builder, not just a status card.

Eligibility Requirements

For Regular Card Variant:

You need a credit score of 750+ and a stable income (salaried or self-employed). Monthly income should be at least ₹50,000 for approval consideration. If you already hold an IDFC unsecured credit card, your new IndiGo card shares that existing credit limit – it doesn’t add a separate one. Documents needed: PAN card, Aadhaar, recent salary slip or income proof, address proof, and bank statements (last 6 months).

For FD-Backed Variant:

No credit check required at all. Simply pledge a ₹1 lakh fixed deposit with IDFC FIRST Bank and your credit limit equals that amount. This route works for students, first-time credit card users, or anyone rebuilding their score. Documents needed: PAN card, Aadhaar, address proof, and the FD created during application.

Final Verdict

This card actually replaces the Vistara offering pretty well. While IndiGo and Air India now match domestic coverage, this card finally justifies its ₹5,000 fee.

The 4%+ return is genuine. The fee gets offset by vouchers. And if you reach Blu 1 tier, returns touch 4.4%+.

The missing lounges sting a bit. But at these reward levels, you’re not just paying for the card – you’re actually profiting from it.

If you fly IndiGo regularly or spend big, this card is a no-brainer. Your ₹5,000 annual fee becomes an investment that pays back ₹24,000+ in rewards.

That’s not marketing talk. That’s math.