IndiGo Axis Bank Credit Card Review 2026: Is This the Best Travel Card for IndiGo Flyers?

Two new IndiGo Axis Bank credit cards are here - but which one suits a middle-class Indian family? Our detailed review covers reward rates, milestone targets, and honest return calculations.

CARD REVIEWS

Kapil

2/19/20264 min read

Axis Bank has finally joined the IndiGo BluChip party. On February 18, 2026, the two brands launched not one but two co-branded credit cards. IndiGo already had tie-ups with Kotak, SBI, and IDFC First Bank. But this one is different – Axis Bank was formerly IndiGo’s partner airline Vistara’s biggest banking ally. So this launch was quietly anticipated by frequent flyers and points enthusiasts alike.

No Air India co-branded card is on the table for Axis Bank right now. Air India’s credit card partnerships remain separate, and this tie-up is firmly in IndiGo’s corner.

Two Cards, Two Very Different Audiences

The IndiGo Axis Bank Credit Card costs ₹799 plus GST and is aimed at regular travellers who fly IndiGo two to four times a year. The IndiGo Axis Bank Premium Credit Card is priced at ₹5,000 plus GST and is built for frequent flyers who want airport lounge access, better forex rates, and higher reward rates.

Both cards run on RuPay and Visa networks. The rewards currency is IndiGo BluChips – a point system you can redeem only on IndiGo flights. One BluChip roughly equals ₹0.50 in flight value on popular routes, though redemption value varies.

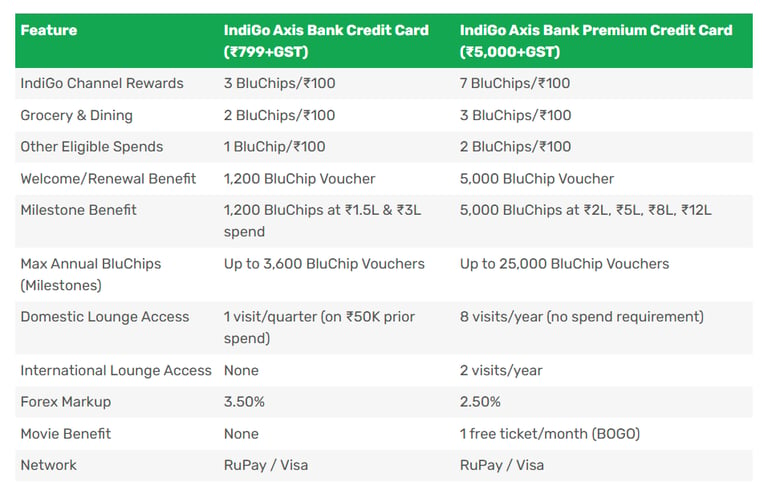

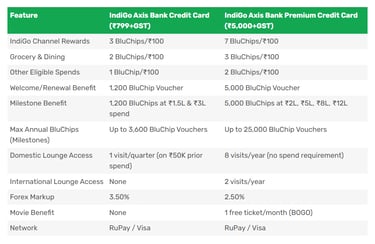

Reward Structure – What You Actually Earn

Here is how the two cards stack up across key parameters:

Milestone Maths – When Does It Get Interesting?

The Standard card gives you a 1,200 BluChip voucher when you spend ₹1.5 lakh and ₹3 lakh in a card year – totalling up to 3,600 BluChip vouchers including the annual benefit. That is about ₹1,800 in flight value – barely covering the card fee and GST.

The Premium card is a different story. Milestone bonuses of 5,000 BluChips each kick in at ₹2 lakh, ₹5 lakh, ₹8 lakh, and ₹12 lakh annual spends. Add the joining/renewal 5,000 BluChips and you can stack up to 25,000 BluChip vouchers a year. At ₹0.50 per BluChip, that is ₹12,500 in flight credit – making the ₹5,000 fee look reasonable for a high spender.

The BluChip programme also has tiers – though Axis Bank has not yet fully detailed how card spends interact with BluChip Gold or Platinum tier status. Higher BluChip tiers typically unlock better redemption options and priority boarding on IndiGo, so card holders who also fly frequently may benefit twice over.

The Lounge Access Catch You Need to Know About

Here is the fine print that matters. On the Standard Card, the one quarterly domestic lounge visit is NOT free upfront. You must spend ₹50,000 in the preceding three months to unlock it. So if your previous quarter’s spends fell short, you pay at the lounge door.

This is exactly the model IDFC First Bank used with its IndiGo card, which costs ₹4,999 plus GST. The difference? IDFC First offers no lounge access at all – not even spend-gated. For ₹4,999, the absence of any lounge access on the IDFC card was widely criticised. Axis Bank’s premium card fixes this properly: 8 domestic and 2 international visits are included without monthly spend conditions attached. That is the right call for a card at this price point.

Another advantage over IDFC First: Axis’s premium card charges 2.5% forex markup versus IDFC First’s 1.49%. IDFC wins on forex. But Axis wins on lounge access, rewards on groceries, and the movie benefit – categories that matter more to the average Indian family.

Fees, Charges, and How to Apply

Standard Card Annual Fee: ₹799 + GST (approximately ₹943)

Premium Card Annual Fee: ₹5,000 + GST (approximately ₹5,900)

Add-On Card: Details to be confirmed; typically at reduced or zero fee

Excluded Categories: Government services, insurance, utilities (including telecom), rent, fuel, jewellery, and wallet loads do not earn BluChips.

UPI Spends: The Standard Card offers accelerated BluChips on UPI transactions – a useful edge for daily spends.

You can apply through Axis Bank’s website or app directly. Axis Bank also offers an FD-backed version of select credit cards for applicants who do not meet income eligibility criteria. If your credit profile is new or thin, a fixed deposit of a defined minimum amount (typically ₹20,000 – ₹25,000 with Axis Bank) lets you get a secured card with the same basic features. The IndiGo IDFC First card also offers an FD-backed route – a growing trend in the co-branded card space.

Who Is Eligible?

Axis Bank has not published exact income thresholds for these cards yet. Generally for the Standard Card, a minimum income of ₹3-4 lakh per annum is expected for salaried applicants. For the Premium Card, expect a minimum annual income of ₹6–8 lakh. You must be between 21 and 60 years of age, with a good CIBIL score (ideally 700+). Self-employed applicants are eligible. IndiGo BluChip membership is mandatory – you will need to enrol before or during the card application process.

Should You Get This Card?

Get the Standard Card if: You fly IndiGo 2–3 times a year, spend ₹50,000+ per quarter on everyday purchases, and want a low-fee entry into the IndiGo BluChip system. The spend-gated lounge is manageable if you are a consistent spender.

Get the Premium Card if: You fly IndiGo 4 or more times a year, spend ₹2 lakh+ annually on the card, watch movies regularly, and value lounge access without conditions. The maths works in your favour above ₹5 lakh annual card spend.

Skip both if: You fly multiple airlines, want flexible redemptions beyond IndiGo, or prefer cashback. These cards are built purely for IndiGo loyalists.

Final Thoughts

The IndiGo Axis Bank launch matters because Axis Bank brings serious network muscle – a large customer base, strong digital infrastructure, and a track record with travel cards. The Premium Card especially offers a well-rounded package that fixes the lounge access problem the IDFC First card was criticised for.

The Standard Card’s spend-gated lounge is its weakest point. Everything else – the UPI rewards, the grocery multiplier, the milestone vouchers – is fairly competitive. For a family like Rahul’s, the premium card delivers real money back, not just marketing fluff.

Watch out for the excluded categories list. Fuel, utilities, rent, and insurance – four of the biggest monthly outgoings for most Indian families – earn nothing. Plan your spends accordingly.