HSBC RuPay Cashback Credit Card Review 2025: Complete Guide & Benefits

Fees, rewards, lounge access, UPI tricks, pros & cons, and how to apply. Is it worth ₹499? Read in 5 min.

CARD REVIEWS

Kapil

7/16/20253 min read

Imagine a shiny new card that rewards you for groceries, late-night take-out, and even that cheeky Paytm bill payment you keep putting off. HSBC just dropped the RuPay Cashback Credit Card, expanding its Indian lineup beyond the classic Visa and Mastercards. If you’ve been waiting for an HSBC card that plays nicely with UPI and lounge visits, here’s your low-down.

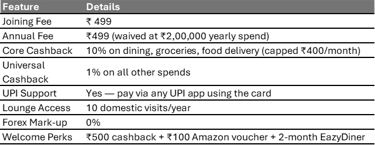

Quick Snapshot

Why Another HSBC Card Matters

I’ve used HSBC’s Platinum cards for years. Good service? Yes. But no seriously rewarding cashback card—until now. This RuPay launch signals HSBC’s push to woo younger, UPI-first shoppers. For folks who skipped HSBC due to limited reward variety, this card plugs that gap.

Benefits & Rewards

1. Chunky 10% Category Cashback

Swipe (or tap via UPI) on groceries, Swiggy/Zomato, and restaurants. The bank credits up to ₹400 every month—so aim for ₹4,000 category spend monthly for max value. Anything more just earns the flat 1%.

2. Forever-On 1%

No hoops. Petrol, gadgets, Netflix—everything not in the bonus trio nets 1%. It’s low compared with specialized cashback cards, but pairs nicely with the 10% slab.

3. UPI Integration

Link the RuPay variant on your favorite UPI app. Scan a kirana QR, split rent, or pay the veggie guy—earn cashback exactly like a card swipe. For me, that’s game-changing; my wallet stays home.

4. Lounge Access & Travel Extras

Ten free domestic visits a year. That’s almost one every other month. Add 0% forex mark-up and you’ve got a viable international companion—just remember, overseas merchants must accept RuPay (many don’t yet).

5. Partner Discounts

10% off Swiggy Instamart (min ₹500, capped ₹200)

5% off Paytm utility bills (min ₹299, cap ₹150)

Cleartrip flight+hotel cuts up to ₹6,000

Nice cherries, not game-changers.

Milestone Sweetener

Spend ₹10,000 in the first 30 days, then download HSBC’s app: bag ₹500 cashback. Complete online Video KYC and you also pocket a ₹100 Amazon voucher. Easy win.

Annual Return Math

Assume monthly outgo:

Dining/Grocery/Food delivery: ₹4,000

Other spends (fuel, OTT, etc.): ₹8,000

That’s ₹12,000 per month or ₹1,44,000 yearly.

Cashback:

Bonus 10% = ₹400×12 = ₹4,800

Flat 1% on ₹96,000 = ₹960

Total = ₹5,760.

Effective return: 5,760÷1,44,000=4.0%

If you breach ₹2,00,000 yearly, the ₹499 fee disappears and net return inches to 4.3%. Not bad for a no-nonsense card.

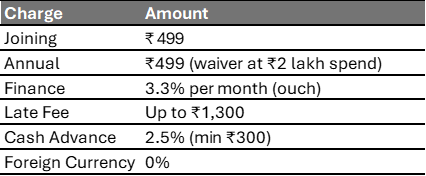

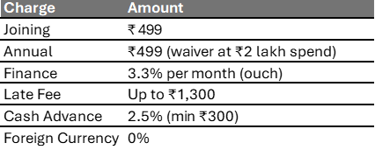

Fees & Charges

Always pay in full; interest bites harder than a Delhi summer.

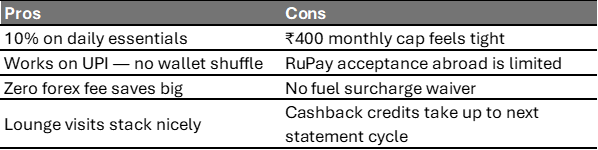

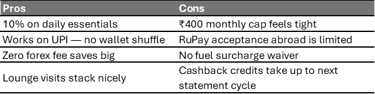

Pros & Cons

Eligibility & Application Twist

You need:

Age 18-65, Indian resident, ₹4 lakh+ salary

Live in select 15 cities

How to Apply (When It’s Back)

Visit HSBC India’s RuPay card page.

Punch basic details; keep PAN & Aadhaar handy.

Schedule & finish a 5-minute Video KYC.

Receive digital card instantly (sometimes) and physical card in 5-7 days.

Tip: Spend ₹10k inside a month to trigger that ₹500 cashback.

Link to the website: https://www.hsbc.co.in/credit-cards/products/rupay-cashback-credit-card/

My Take

I’ll be honest—₹400 monthly cap irks me. But pair the 10% with UPI freedom and lounge access, and it still beats many ₹500-fee cards. If your staple spend is groceries and Swiggy, this card pulls its weight. Frequent fliers might stock a Visa or Mastercard for global swipes, though.

Bottom line:

The HSBC RuPay Cashback is a smart starter or secondary card, geared for digital-savvy shoppers who live on UPI and love a free airport latte. Keep spends disciplined, and you’re banking 4-5% back without sweating complicated reward charts.

And hey, who knew paying your electricity bill could feel this satisfying?