Federal Bank’s New Credit Card Interest Rate: What Changes from January 10, 2026

Federal Bank's 2026 credit card rate revision eliminates ultra-low 8.28% APR. Is maintaining high balance still worth it? Full analysis.

BLOG

Kapil

11/5/20252 min read

Federal Bank just pulled off a move that’ll make high-balance customers sit up and take notice. Starting January 10, 2026, the bank is overhauling how it charges interest on credit cards. And here’s the twist – if you’re parking big money in your account, you’re about to pay a lot more.

What’s Changing?

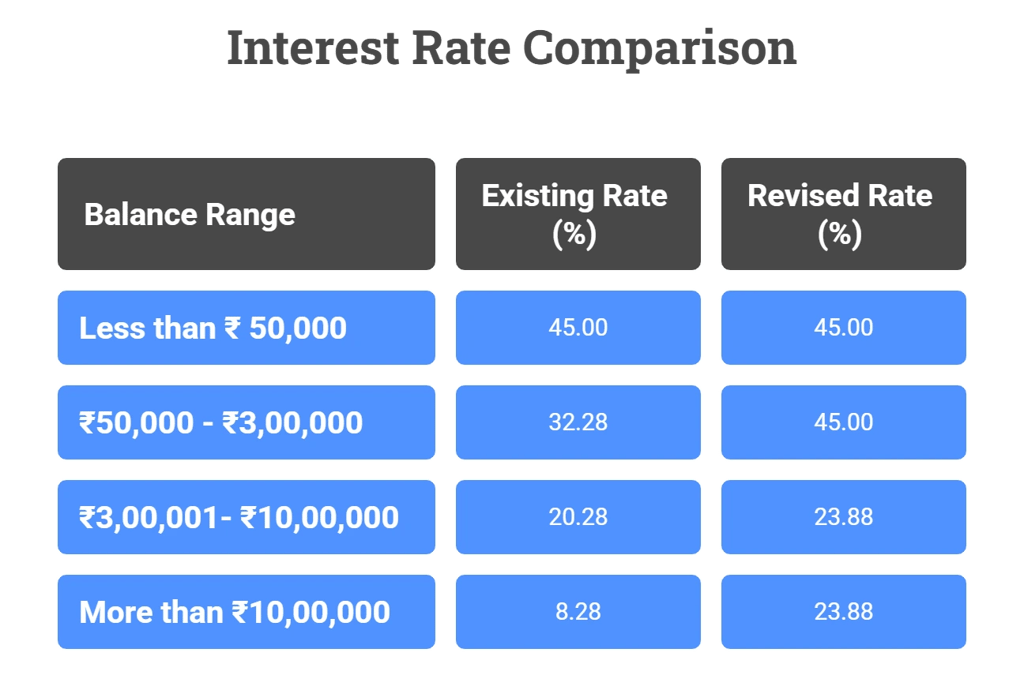

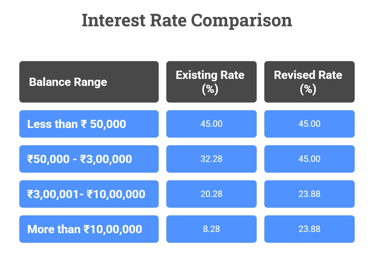

The bank is revising its APR based on your Average Monthly Balance (AMB). The biggest hit? Anyone with over Rs 10 lakh of AMB sees rates nearly triple. Here’s the new rate card:

Why This Change?

Federal Bank is standardising its pricing. An 8.28% APR was nearly charitable compared to most banks charging 36-52%. High balances don’t guarantee low credit risk if customers revolve debt continuously. The move also boosts interest income as credit card debt in India crosses Rs 2.9 lakh crore.

Should You Pull Your Money Out?

Here’s the catch: The Rs 3 lakh to Rs 10 lakh bracket now gets the same 23.88% rate as balances over Rs 10 lakh. So parking Rs 25 lakh makes no sense when Rs 4 lakh gets you identical credit card rates.

If maintaining a high Federal balance was purely for credit card savings, reconsider. Move excess funds to fixed deposits (7%) or liquid mutual funds. Keep just enough – around Rs 3-10 lakh – to get the best available rate without locking up crores.

How the Quarterly Update Works

Your APR updates on the 10th of each quarter based on the previous quarter’s balance:

10th Jan: Based on Oct-Nov-Dec balances

10th Apr: Based on Jan-Feb-Mar balances

10th Jul: Based on Apr-May-Jun balances

10th Oct: Based on Jul-Aug-Sep balances

Federal Bank averages your entire quarter, not just end-of-month balances. Dumping cash in the last week won’t help.

What to Do Now

Pay in full. Interest rates don’t matter if you never carry balances.

Move debt elsewhere. Balance transfer cards offer 0% for 3-6 months. Shift your balance and clear it during the promo.

Convert to EMI. A Rs 1 lakh balance locked into 12-month EMI at 15-18% beats 23.88% monthly interest.

Track your AMB. Staying just below a slab threshold – keeping Rs 3.1 lakh instead of Rs 2.9 lakh—could drop your rate from 45% to 23.88%.

Non-account holders, beware. If you hold a Federal credit card without a savings account, you’re automatically locked into 45% APR.

The Bottom Line

This isn’t unique to Federal Bank. Indian banks are capitalising on higher margins as RBI doesn’t cap credit card rates. Until regulation steps in, expect more rate hikes.

Maintaining high balances no longer guarantees low credit card rates. The days of 8% APR are done. Run your numbers. Shift your balances. And if you can’t pay in full – reconsider carrying credit card debt at all.